Double Materiality Assessment

Double Materiality Assessment

With the Corporate Sustainability Reporting Directive (CSRD) [link to CSRD page] coming into force, the environmental, social and governance information that companies have to report on has become significantly more extensive. In order to decide which sustainability matters are material to report on it is mandatory to carry out a double materiality assessment. However, a double materiality assessment is more than a compulsory step in sustainability reporting; it offers valuable input for any company's strategy.

What is Double Materiality?

The term materiality originates from financial accounting. In accounting, materiality refers to the principle that all transactions or business decisions that are likely to impact investors’ decision-making must be reported on in a business’s financial statements. In sustainability reporting materiality is broader; what is material is based on two perspectives: impact and financial.

- Impact materiality considers how a company’s activities, products and services affect the environment, people, and the economy.

- Financial materiality refers to the impact sustainability topics have on the company.

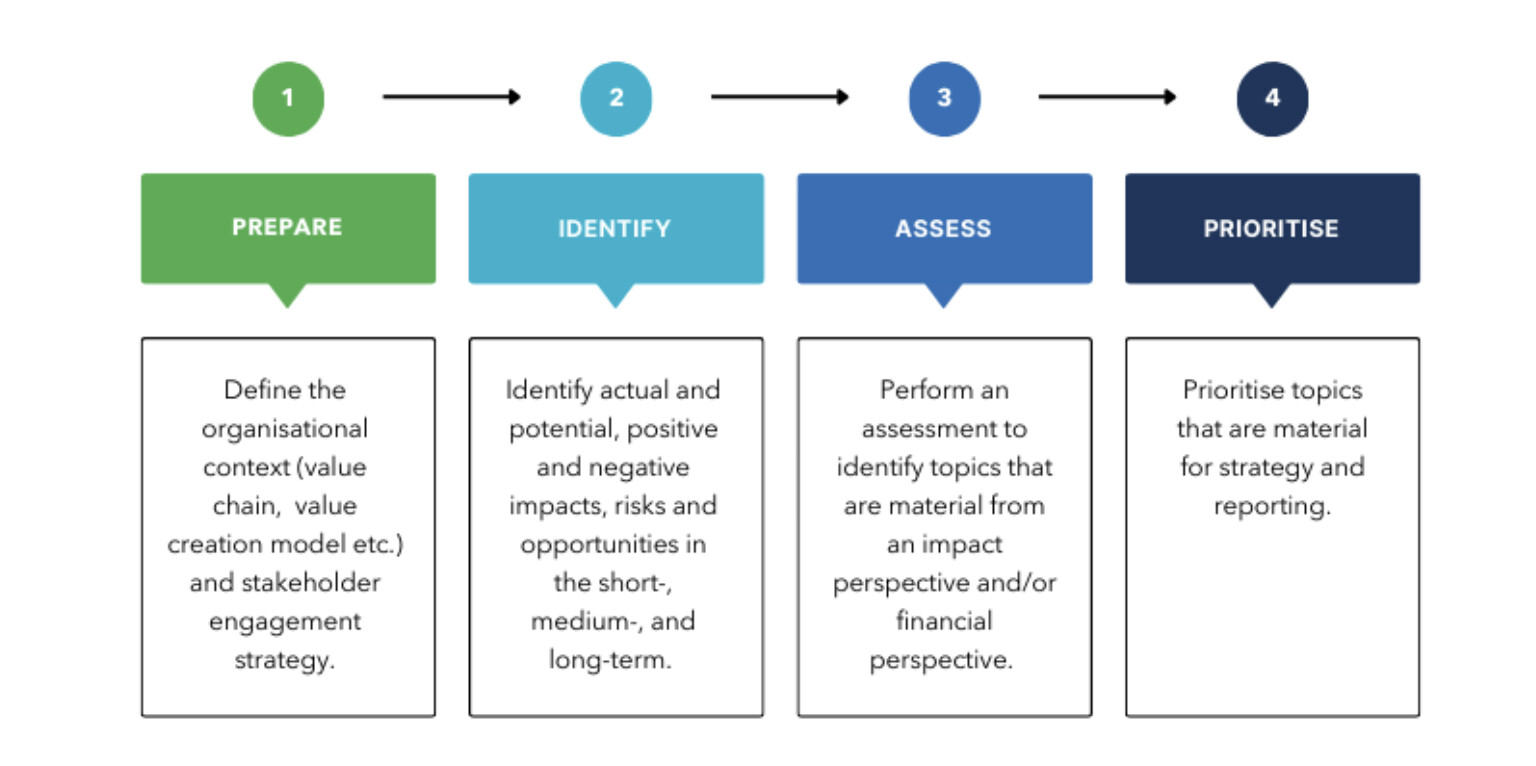

Our approach to double materiality

Setting up a double materiality assessment for the first time can be a real challenge. At 2Impact we have developed a four-step approach to conducting a double materiality assessment, that ensures that you follow all the necessary steps to be audit ready.