The Omnibus – what does it include and what does it mean for companies?

On February 26, 2025, the European Commission published its proposal for the first Omnibus Simplification Package. The proposal features several adjustments and simplifications to key pieces of sustainability legislation. Changes have been proposed to the CSRD, EU Taxonomy, CSDDD, and CBAM. In addition, the Commission has proposed amendments to several investment programmes including InvestEU, EFSI, and legacy financial instruments. What do these changes include and what do they mean for companies?

Legislative process

The proposed adjustments have been put forward by the European Commission and are now under review by the Council of the European Union (Member States) and the European Parliament, each of which will form its own position. The three institutions—the Commission, Council, and Parliament—will then negotiate to reach a final compromise. Once an agreement is reached, it will be published in the Official Journal and be formally adopted.

The European Commission has called on the co-legislators to fast-track the negotiations, especially to provide clarity for companies currently required to report for the first time in 2026 for FY2025. To do so, they have included in the proposal that Member States should transpose it into national legislation by 31 December 2025.

How fast (or slow) the negotiations will go in practice is difficult to say, normally a fast process takes 1-1.5 years, but here we could see around 6-8 months. It all comes down to how willing the political groups in the European Parliament and the Member States are to compromise and which alliances that can be built.

Changes to the CSRD

Scope and implementation

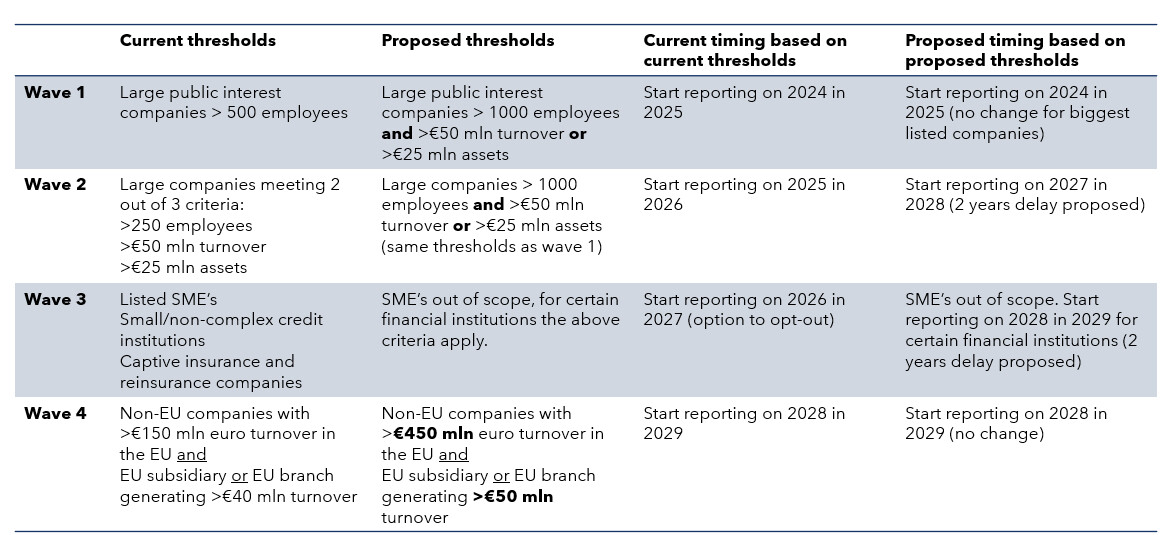

The main proposed adjustment to the CSRD is a substantial reduction of the scope. In the proposal, the CSRD reporting requirements would only apply to large companies with more than 1000 employees and either a turnover above EUR 50 million or a balance sheet above EUR 25 million. This would reduce the number of companies in scope by around 80%. The implementation of the CSRD is also proposed to be delayed for two years for companies currently in the scope of CSRD that are required to report as of FY2025 or FY2026.

European Sustainability Reporting Standards (ESRS)

While the concept of double materiality remains at the core of the CSRD, the European Commission intends to adopt a delegated act to revise the first set of ESRS as soon as possible and at the latest six months after the entry into force of the Omnibus Directive. The revision of the delegated act will substantially reduce the number of mandatory ESRS datapoints by:

- Removing those datapoints deemed least important for general purpose sustainability reporting;

- Prioritising quantitative datapoints over narrative text; and

- Further distinguishing between mandatory and voluntary datapoints, without undermining interoperability with global reporting standards and without prejudice to the materiality assessment of each undertaking.

In addition to these simplifications, the European Commission will no longer develop sector-specific ESRS standards in the future. For companies outside of the new CSRD-scope, a new standard will be developed by EFRAG based on the current VSME standard.

Value chain cap

The proposal includes an extended and strengthened value chain cap to ensure that sustainability reporting requirements on large companies do not burden smaller companies in their value chains. This cap would protect all undertakings with up to 1000 employees from receiving disproportionate information requests, rather than just SMEs as is currently the case. The limit would be defined by the new voluntary standard that will be adopted by the Commission and developed by EFRAG. While that is being developed, the Commission intends to issue a recommendation on voluntary sustainability reporting as soon as possible.

Assurance

The possibility of moving from a requirement for limited assurance—a lower level of confidence by assurance providers, obtained by performing less extensive audit activities—to a requirement for reasonable assurance—higher level of confidence by assurance providers, obtained by performing more extensive audit activities—is proposed to be removed. This aims to provide certainty that there will be no future increase in assurance costs for companies in scope.

In addition, the obligation for the European Commission to adopt standards for sustainability assurance by 2026 has been replaced by a requirement for the European Commission to issue targeted assurance guidelines by the same year. While the extent of assurance guidance remains unclear at this moment, the objective of the European Commission is to address emerging assurance issues more quickly and create more flexibility in assurance requirements to prevent generating unnecessary burdens on the reporting companies.

How does the Omnibus proposal affect CSRD reporting?

One of the main uncertainties is how the updated scope and delayed implementation of the CSRD will impact different companies. In short, our analysis is:

Member States that have not yet transposed the CSRD into national law (this includes for example the Netherlands and Germany)[1]

It is unlikely that these Member States would push for transposition of the CSRD before the Omnibus proposal is fully negotiated with a final agreement in place, given the additional legal uncertainty that this would create. That being said, there is of course nothing preventing them from doing so. We could expect these Member States to make public indications in the coming weeks and months about their plans. This is for example what the Dutch government is doing.

Member States that have transposed the CSRD into national law[2]

- First wave: companies required to report under the CSRD over FY2024 (public interest entities[3] with more than 500 employees) - if the Omnibus stays in its current form, the companies that have fewer than 1000 employees would be out of scope for subsequent years.

- Second wave: companies required to report under the CSRD over FY2025 (two out of three criteria: 250 employees, turnover exceeding EUR 50 million per year, and a balance sheet total of more than EUR 25 million) - if the Omnibus stays in its current form, the companies that have fewer than 1000 employees would be out of scope. For companies with more than 1000 employees, there could be a delay in implementation (first report FY2027) if this proposal is kept in the negotiations. Depending on when the co-legislators can agree on the delayed implementation, these companies might have to report over FY2025.

- Third wave: companies required to report under the CSRD over FY2026: listed SMEs - if the Omnibus proposal stays in its current form, the listed SMEs will be out of scope. There is technically a possibility that they could have to report over FY2026 of the Omnibus proposal is not agreed upon by then.

As with the Member States that have not transposed the CSRD, we can likely expect governments to publicly indicate their plans in the coming months, i.e. whether they intend to impose the CSRD reporting (especially for wave 2 companies) in the coming weeks and months.

Changes to the EU Taxonomy

Scope

The scope of the companies mandated to report in line with the EU Taxonomy is proposed to be significantly reduced. With the Omnibus, only companies with more than 1000 employees and with a turnover of more than EUR 450 million would need to report. This would bring the scope of the EU Taxonomy more in line with the CSDDD, and it is also more in line with the proposed adjusted scope of the CSRD.

Voluntary reporting

The European Commission also proposes to introduce an opt-in for companies that are not in scope. With this opt-in, companies that do not exceed a net turnover of EUR 450 million can report on activities that are aligned or partially aligned with the EU Taxonomy with the idea of fostering a gradual environmental transition of activities over time. When reporting companies would need to disclose KPIs related to turnover and CapEx, and may disclose the KPI related to OpEx.

Changes to the delegated acts

The proposal included an amendment to the EU Taxonomy Disclosures Delegated Act, Climate Delegated Act, and Environmental Delegated Act. There is a public consultation open, where anyone can provide input, until 26 March. The main changes introduced are a financial materiality threshold of 10%, simplification of the mandatory reporting tables (reducing them from three to one), and simplification of the most complex “Do no Significant harm” (DNSH) criteria for pollution prevention and control related to the use and presence of chemicals that apply horizontally to all economic sectors under the EU Taxonomy (Appendix C).

Changes to the CSDDD

The Omnibus proposes significant simplifications to the due diligence requirements in the CSDDD. For example, companies would now only need to focus their due diligence efforts on their direct business partners.

In addition, companies would need to direct their focus on direct business partners with over 500 employees, limiting the amount of information that may be requested from SMEs and SMCs as part of the value chain mapping by large companies. Companies in scope of the CSDDD would also only need to monitor their business partners once every 5 years instead of annually, with ad hoc assessments where necessary. In addition, the requirement to consider termination of the business relationship as a last resort in case of non-compliance has been removed in the Omnibus proposal.

While stakeholder engagement will remain a key part of the due diligence process, the definition of stakeholders has been narrowed to only include individuals and communities that could be directly affected by a company's or its business partners’ conduct. This would for example exclude consumers and NGOs. The current civil liability provisions of the CSDDD will be deleted and left to the discretion of Member States.

Finally, the Omnibus proposes a delay in implementation of the CSDDD. Large companies would now need to start complying from 26 July 2028. The adoption of guidelines has also been delayed by one year to July 2026.

Changes to CBAM

A new cumulative annual threshold of 50 tonnes per importer is proposed, which will exempt around 182,000 importers, mostly SMEs and individuals, from CBAM obligations. According to the European Commission, this will eliminate reporting requirements for around 90% of importers while still covering 99% of emissions.

For companies that remain in scope of CBAM, the proposal simplifies authorisation and reporting requirements, with the aim of making compliance more straightforward. It also strengthens measures to prevent circumvention and abuse, ensuring CBAM remains effective in the long term. This streamlining comes ahead of a planned extension of CBAM to other ETS sectors and downstream goods, with a new legislative proposal on scope expansion expected in early 2026.

How can you approach these changes?

As sustainability regulations continue to evolve, accountability and transparency are fundamental for doing business in a responsible way. Proactively engaging in sustainability reporting and due diligence contributes to risk management, better positioning to meet stakeholder expectations seeing that investors and partners increasingly rely on this information to assess performance, as well as talent attraction.

What can you do more practically?

While there is no one size fits all advice, companies can take the following steps to define how they will act:

- Assess the impact of the changes on your company

- Are we still in scope of the CSRD/EU Taxonomy/CSDDD/CBAM if this Omnibus Package is adopted?

- Will we face a delay if this Omnibus is adopted? - Define different scenarios and related actions

- Consider your ambition and stakeholder expectations

- Consider where you are right now in your journey

- Consider risks (of non-compliance) and opportunities - Determine preferred scenario(s) and if relevant, update your roadmap(s)

While for some companies the need to comply (in the short-term) is likely gone there are many reasons to keep going. For many companies in the second wave the extra time brings opportunities. Instead of being in a rush to report, there will be time to create awareness and understanding within your organisation, and to identify the most material ESG topics and to create your ESG strategy. At the same time, setting up a system for collection of quantitative data takes time. So, use your extra time wisely. If you are not in scope anymore, we advise you to have a look at the VSME standard already and to see how reporting based on this much lighter standard could be beneficial for you.

If you would like to talk about how the Omnibus Simplification Package will affect your company and how you can develop your plan of action, do not hesitate to reach out to us at esther@2impact.nl.

--------

[1] At the time of writing this blog, the following 8 countries had not transposed the CSRD into national law: AT, CY, DE, ES, LU, MT, NL, and PT.

[2] At the time of writing this blog the following 19 countries had transposed the CSRD into national law: BE, FR, IT, PL, HU, SK, CZ, BG, RO, LT, EE, LV, FI, SE, IE, HR, DK, SI, and EL.

[3] Public interest entities mean entities that are: i) governed by the law of a Member State and whose transferable securities are admitted to trading on a regulated market of any Member State (in broad terms listed companies) ii) credit institutions iii) insurance undertakings iv) designated by Member States as public interest entities