Maturing the double materiality assessment (DMA)

Many large listed and non-listed companies have performed their first double materiality assessment (DMA) to comply with the Corporate Sustainability Reporting Directive (CSRD). But what to do with the outcomes of the DMA? The first point is obvious, the DMA is a requirement to identify the material topics (and their related impacts, risks and opportunities) which need to be reported on in the annual report, as a part of the sustainability statement. However, the DMA is more than just a requirement to tick the boxes to comply with the CSRD. It can be used for many other things, such as:

- A solid basis for your ESG strategy: The DMA shows your most important material Environmental, Social and Governance (ESG) topics and thus can guide you in developing or updating your (ESG) strategy. It provides a clear focus on the topics that matters most.

- Alignment with internal processes: It is a best practice to align your DMA with other internal processes such as your enterprise risk management (ERM) or due diligence process. The integration of your DMA with other organisational processes streamlines the in- and outflow of information and embeds sustainability with business.

- A starting point to develop ESG policies and action plans: Policies and action plans should be your guide in your approach to mitigate impacts and risk and to capture opportunities. A DMA can help you identify which topics your company needs to have a policy and action plan on to manage its related impacts, risks, and opportunities

- A way to improve your stakeholder engagement: Companies and stakeholders influence each other; this can be positively or negatively. Therefore, it is important for the company to regularly engage with its stakeholders so they can express their concerns or needs. The DMA is the perfect moment to let your stakeholders express their voices and strengthen the relationships with them. It can also bring valuable ideas on how you can work on managing your impacts, risks, and opportunities.

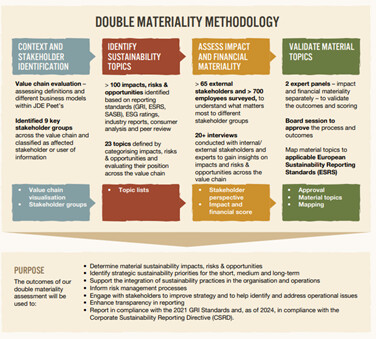

For example, JDE Peets is a frontrunner in using their DMA for more than only compliance:

Source: JDE Peet's annual report 2023, p. 17

How frequently should you update your DMA

An extensive review of your DMA should be aligned with the strategy cycle, which is typically 2-4 years. This should be complemented with a light update each year. This light review gives you the chance to align your DMA with new best practices or incorporate feedback from your auditor or stakeholders. This light review can entail many things, below we explain how you can do a light review step by step.

If major changes have emerged such as new subsidiaries, new activities, new business model, etc. it is strongly recommended to redo your DMA instead of doing a light review.

How to conduct a DMA light review

At 2Impact we conduct a DMA following four key steps: 1) Setting up the organisational context, 2) Identifying IROs, 3) Assessing the IROs and 4) Prioritising and validating the IROs.

Below is an explanation of what a light review could entail for each of the steps.

1) Setting up the organisational context

During the light review it is recommended to see if anything has changed related to your organisational context, considering the following:

- Has your business model changed? (e.g. new activities, new markets, new products)

- Has your organizational structure or value chain changed? (e.g. (dis)investment in subsidiaries, joint ventures, etc.)

- Have you mapped out all relevant activities and actors within your value chain clearly? If not, then this should be done. If any changes have been made in your value chain this should also be updated. A good value chain mapping is needed so it will be easier to link IRO’s and topics to the value chain activities and actors.

- Have new laws or regulations been introduced or drafted that could impact your business activities?

- Have new trends or developments emerged that could impact your business activities?

- Have new stakeholder groups emerged or has one group become more important?

In their annual report of 2024 Netcompany shows their approach of a light review, with the first step being to revisit their organisational context.

2) Identifying IROs

The next step would be to check if any new impacts, risks, or opportunities have emerged. This can be based on new scientific or technical research or market study that has been done internally or externally, internal processes such as Due Diligence, changes in your organisational context or by comparing your IROs with the IROs of your peers that can be found in their annual reports. If previous IROs need to be sharpened or reformulated (e.g. specifying the activities, revisiting time horizons, etc.) this can also be done.

In some cases, we see that companies focused on identifying material (sub-) topics, instead of IROs (e.g. due to reporting in accordance with the GRI Sustainability Reporting Standards). If no IROs have been previously formulated, then IROs should be identified per each material (sub-)topic.

If you have involved your stakeholders in your first DMA you can always think about involving more internal or external stakeholders to validate your existing IROs. If you have not involved your stakeholders in your previous DMA, then now is the right time to do so! These insights from your different stakeholder groups can provide valuable information and improve your stakeholder engagement all at once. We recommend involving your stakeholders through either focus groups or one-on-one interviews.

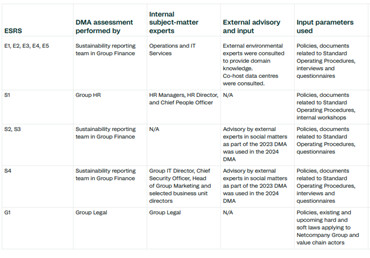

In their annual report of 2024 Netcompany provides a nice overview on which internal and external experts were involved during the DMA.

3) Assessing IROs

As with the identification step, you can choose to involve (more) stakeholders in the scoring assessment of the IROs. We always recommend involving internal and/or external experts who have a good knowledge about ESG topics or of the company activities.

When revisiting your scoring, it is highly recommended to take the following points into account:

- Were the scores of the IROs (including argumentation) based on (scientific) research? If not, it can be a good exercise to try and base your scoring on (quantitative) research instead of opinions. This is where involving experts can be quite useful!

- Was your scoring done by taking into account mitigation measures? If yes, then revisit your scoring and score the IRO without thinking of the mitigation measures you have put in place or which are planned. This is crucial and can have a significant impact on your scoring and thus the materiality of your topics. Scores should be assessed on a “gross” basis. This approach helps identify which IROs and, by extension, which topics are truly important within your sector and your value chain. For example, in the construction sector, safety is a key priority. However, if you were to evaluate the impact and risk of workplace accidents while factoring in all mitigation measures in place, the IRO (and possibly the topic itself) might no longer appear material. Nevertheless, stakeholders, such as clients, still expect construction companies to report on this. Afterall, it is not for nothing that construction companies put so much effort into managing their IROs related to health and safety, and this should be communicated.

- When revisiting scoring of your impacts, it is good to double check if all your potential impacts are still potential. If they became actual in the past year, then the scoring criteria changes as well.

- When scoring the magnitude of the financial effects (one of the two scoring criteria for risks and opportunities) was the cumulative effect taken into account? If no, then revisit your scoring for risk and opportunities and try quantifying what the cumulative magnitude of the financial effect would be, taking into account the time horizons (short, mid, long-term) linked to the risk or opportunity.

4) Prioritising and validating IROs

If any changes occurred in the previous step and this has led to updated scorings of the IROs, double check if this leads to new changes in reporting requirements. This can be done by “in-scope” analysis against the ESRS disclosure requirements. Finally, do not forget to validate the new DMA with the management board or a similar body which is responsible for the outcomes of the DMA.

All changes made to the methodology and the outcomes of the DMA should be stated clearly in the DMA methodology paper, which can be used as an audit memo as well. Another suggestion from 2Impact would be to create a DMA policy, containing the “static” information, including e.g. time horizons, approach to scoring, approval and validation process, etc. Each year, once you have done a (light) update of the DMA, the resulting IROs would be the “dynamic” part of the policy documentation. We see this as a frontrunner practice that helps companies to align their DMA process with others such as their Due Diligence and ERM.

As mentioned before, your DMA should receive a quick revision every year to update it based on the latest changes and best practices.

Dynamic materiality

Another trend we observe is dynamic materiality which refers to how material topics evolve or change over time, either in terms of significance or the nature of the impact. This concept emphasizes the need for continuous reassessment of your DMA outcomes.